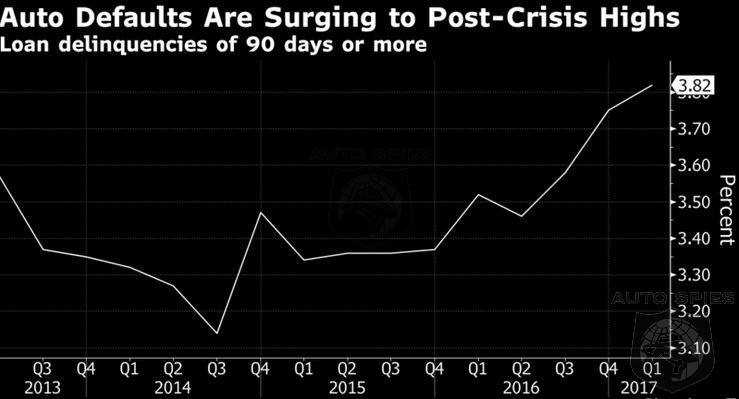

Subprime Loans Defaulting At Record Rates - Will The Next Recession Be Triggered By The Auto Industry?

It’s classic subprime: hasty loans, rapid defaults, and, at times, outright fraud.

Only this isn’t the U.S. housing market circa 2007. It’s the U.S. auto industry circa 2017.

A decade after the mortgage debacle, the financial industry has embraced another type of subprime debt: auto loans. And, like last time, the risks are spreading as they’re bundled into securities for investors worldwide.

Subprime car loans have been around for ages, and no one is suggesting they’ll unleash the next crisis. But since the Great Recession, business has exploded. In 2009, $2.5 billion of new subprime auto bonds were sold. In 2016, $26 billion were, topping average pre-crisis levels, according to Wells Fargo & Co.

Read Article

Copyright 2026 AutoSpies.com, LLC